Effort Alone Won't Scale a Brokerage.

Build the System.

Most agents are stuck on a treadmill. Buy leads, dial, hope, repeat. We do something different. We build the entire lead gen system for you across Final Expense, IUL, or annuities. We're an S-corp, so we get paid when you produce. If you don't make money, we don't make money. That's the deal.

Apply NowInvite-only. Two minutes. We take the risk, you take the upside.

Look. The problem isn't your effort. The problem is the model. The model is broken. Like Sisyphus, the harder you push, the further behind you fall. Calling lists. Buying leads. Burning cash. There's only one way out: stop renting your income. Start owning the system.

Buying Leads = Renting Income

Vendors mark up 5x and sell shared, recycled contacts. You stop paying, the leads stop. Nothing compounds. Nothing scales. You're renting the boulder, then pushing it for free.

Dials Don't Compound

Every call is a one-time effort. Hours = dollars. Stop dialing, stop earning. No asset gets built behind the work. You're trading hours for boulders.

The Personal Ceiling

Your business is bottlenecked by the hours you can personally work. Without a system, scale is mathematically impossible. You're not building a business. You're buying yourself a job.

Zero Skin In The Game

Your lead vendor doesn't care if you close. They already got paid. No shared incentive. No partnership. Just a transaction, with 100% of the risk on you.

Here's how this works. Two paths. One is for established producers who can already close. The other is for producers who need the system built with them. Both paths get you to the same place. A business that scales without you carrying the boulder yourself.

Done-For-You Lead Generation

We build, deploy, and run your complete lead gen system for Final Expense, IUL, or annuities, start to finish. We're an S-corp, which means we can legally take performance comp with zero rebaiting risk. Translation: we only eat when you eat. If we don't produce business for you, we don't get paid. That's it.

- Done-for-you ad creative, funnels, and lead gen infrastructure

- Exclusive real-time leads, never shared, never recycled

- S-corp performance comp, zero rebaiting risk, fully compliant

- Skin in the game on us. Real alignment, not a sales pitch

- Built for Final Expense, IUL, and annuity producers

Diversified Lead Flow Coaching

Don't qualify for performance comp yet? Totally fine. We coach you, hands-on, until your lead flow is fully diversified across four channels: paid social, organic, referrals, and blue-ocean/free. The goal: a pipeline that runs without you holding it up at every turn.

- Weekly 1-on-1 coaching with our team, not a Slack channel

- Open group trainings 5 days a week, drop in any time you need them

- Custom funnel + ad system built for your verticals

- Four-channel lead diversification: paid, organic, referral, and blue-ocean/free

- Hands-on accountability until the results actually land

We've been hired by 8 different lead vendors and 5 IMOs to fix their lead quality. So we've seen this game from both sides. The agent buying leads, and the shop selling them. And here's the truth almost nobody says out loud: the service providers are just as burnt out as the agents.

We've all been burned by inflated promises that nobody could actually keep. That's why we don't do insane guarantees. We only take on people we're confident we can actually help. Part of that is being honest about which path fits: us doing it completely for you on performance, or giving you the tools and access to hit that next $15,000 a month in commissions yourself.

We'd rather turn you down than over-promise. That's why both paths exist.

No gimmicks. No upsells. We won't recruit you. Just the four things every life and annuity producer actually needs to scale without buying themselves another job.

Exclusive Lead Flow

Real-time, exclusive leads through paid social. No middleman markup. No shared lists. No aged contacts that have already been worked twice. Yours and yours alone.

Systems That Scale

Custom marketing infrastructure and conversion sequences built specifically for Final Expense, IUL, and annuities. The asset gets built behind the work, not just hours-for-dollars.

Hands-On Partnership

Direct access to our team. We don't hand you a course and wish you luck. We work alongside you until you're producing predictably, not just hopefully.

Skin In The Game

Performance comp on Path 1. Pay-when-you-produce guarantee on Path 2. Either way, our revenue is locked to your results. We win when you win. Period.

2 minutes. No obligation.

Simple: we don't get paid until you do. Acropolis Digital is an S-corp, which means we can legally take performance comp on the lead gen work we deliver. We take a share of the business we generate for you. If we don't produce, we don't get paid. That's the cleanest alignment money can buy.

Performance comp only works when both sides are set up to win. If you can't close, we both lose. So we vet every producer on verticals, licensing, closing capacity, the whole thing. If you're a fit, we move fast. If you're not a fit for performance, we'll tell you on the call. The coaching program may be the path. Either way, you'll know in 30 minutes.

The coaching program is for producers who don't qualify for performance comp yet but want their own diversified lead flow. The deal: do the work, hit $15,000/month in commissions within 180 days, or you keep us free until you do. That's it. We only run a 20-seat cohort. 7 are filled. 13 remain. When the room is full, the room is full.

Exclusive, real-time leads through paid social for Final Expense, IUL, and annuity verticals. No aged leads. No shared leads. They go to you, not recycled from a vendor list. Fun fact: lead vendors hire us to improve the quality of leads they sell to other agents at 5x markup. With Acropolis, you cut them out of the chain entirely.

Licensed Final Expense, IUL, and annuity producers who want a business that scales without grinding harder every month. Performance path: established producers with proven closing capacity. Coaching path: producers who want to build the system themselves with hands-on support and a results-based guarantee. We won't try to recruit you. Even if we wanted to, we can't. Our S-corp is licensed to partner with other agents' LOAs, which means we literally cannot recruit you even if we tried.

Fill out the form below. 2 minutes. We review it, we hop on a call, we figure out which path fits. If it's a fit, we get to work. If it's not, we'll tell you. No obligation, either way.

Fill out the form. 2 minutes. We'll figure out which path fits and reach out within one business day. If it's not a fit, you'll hear that too. Either way, no obligation.

Effort Alone Won't Scale a Brokerage.

Build the System.

Most agents are stuck on a treadmill. Buy leads, dial, hope, repeat. We do something different. We build the entire lead gen system for you across Final Expense, IUL, or annuities. We're an S-corp, so we get paid when you produce. If you don't make money, we don't make money. That's the deal.

Apply NowInvite-only. Two minutes. We take the risk, you take the upside.

Look. The problem isn't your effort. The problem is the model. The model is broken. Like Sisyphus, the harder you push, the further behind you fall. Calling lists. Buying leads. Burning cash. There's only one way out: stop renting your income. Start owning the system.

Buying Leads = Renting Income

Vendors mark up 5x and sell shared, recycled contacts. You stop paying, the leads stop. Nothing compounds. Nothing scales. You're renting the boulder, then pushing it for free.

Dials Don't Compound

Every call is a one-time effort. Hours = dollars. Stop dialing, stop earning. No asset gets built behind the work. You're trading hours for boulders.

The Personal Ceiling

Your business is bottlenecked by the hours you can personally work. Without a system, scale is mathematically impossible. You're not building a business. You're buying yourself a job.

Zero Skin In The Game

Your lead vendor doesn't care if you close. They already got paid. No shared incentive. No partnership. Just a transaction, with 100% of the risk on you.

Here's how this works. Two paths. One is for established producers who can already close. The other is for producers who need the system built with them. Both paths get you to the same place. A business that scales without you carrying the boulder yourself.

Done-For-You Lead Generation

We build, deploy, and run your complete lead gen system for Final Expense, IUL, or annuities, start to finish. We're an S-corp, which means we can legally take performance comp with zero rebaiting risk. Translation: we only eat when you eat. If we don't produce business for you, we don't get paid. That's it.

- Done-for-you ad creative, funnels, and lead gen infrastructure

- Exclusive real-time leads, never shared, never recycled

- S-corp performance comp, zero rebaiting risk, fully compliant

- Skin in the game on us. Real alignment, not a sales pitch

- Built for Final Expense, IUL, and annuity producers

Diversified Lead Flow Coaching

Don't qualify for performance comp yet? Totally fine. We coach you, hands-on, until your lead flow is fully diversified across four channels: paid social, organic, referrals, and blue-ocean/free. The goal: a pipeline that runs without you holding it up at every turn.

- Weekly 1-on-1 coaching with our team, not a Slack channel

- Open group trainings 5 days a week, drop in any time you need them

- Custom funnel + ad system built for your verticals

- Four-channel lead diversification: paid, organic, referral, and blue-ocean/free

- Hands-on accountability until the results actually land

We've been hired by 8 different lead vendors and 5 IMOs to fix their lead quality. So we've seen this game from both sides. The agent buying leads, and the shop selling them. And here's the truth almost nobody says out loud: the service providers are just as burnt out as the agents.

We've all been burned by inflated promises that nobody could actually keep. That's why we don't do insane guarantees. We only take on people we're confident we can actually help. Part of that is being honest about which path fits: us doing it completely for you on performance, or giving you the tools and access to hit that next $15,000 a month in commissions yourself.

We'd rather turn you down than over-promise. That's why both paths exist.

No gimmicks. No upsells. We won't recruit you. Just the four things every life and annuity producer actually needs to scale without buying themselves another job.

Exclusive Lead Flow

Real-time, exclusive leads through paid social. No middleman markup. No shared lists. No aged contacts that have already been worked twice. Yours and yours alone.

Systems That Scale

Custom marketing infrastructure and conversion sequences built specifically for Final Expense, IUL, and annuities. The asset gets built behind the work, not just hours-for-dollars.

Hands-On Partnership

Direct access to our team. We don't hand you a course and wish you luck. We work alongside you until you're producing predictably, not just hopefully.

Skin In The Game

Performance comp on Path 1. Pay-when-you-produce guarantee on Path 2. Either way, our revenue is locked to your results. We win when you win. Period.

2 minutes. No obligation.

Simple: we don't get paid until you do. Acropolis Digital is an S-corp, which means we can legally take performance comp on the lead gen work we deliver. We take a share of the business we generate for you. If we don't produce, we don't get paid. That's the cleanest alignment money can buy.

Performance comp only works when both sides are set up to win. If you can't close, we both lose. So we vet every producer on verticals, licensing, closing capacity, the whole thing. If you're a fit, we move fast. If you're not a fit for performance, we'll tell you on the call. The coaching program may be the path. Either way, you'll know in 30 minutes.

The coaching program is for producers who don't qualify for performance comp yet but want their own diversified lead flow. The deal: do the work, hit $15,000/month in commissions within 180 days, or you keep us free until you do. That's it. We only run a 20-seat cohort. 7 are filled. 13 remain. When the room is full, the room is full.

Exclusive, real-time leads through paid social for Final Expense, IUL, and annuity verticals. No aged leads. No shared leads. They go to you, not recycled from a vendor list. Fun fact: lead vendors hire us to improve the quality of leads they sell to other agents at 5x markup. With Acropolis, you cut them out of the chain entirely.

Licensed Final Expense, IUL, and annuity producers who want a business that scales without grinding harder every month. Performance path: established producers with proven closing capacity. Coaching path: producers who want to build the system themselves with hands-on support and a results-based guarantee. We won't try to recruit you. Even if we wanted to, we can't. Our S-corp is licensed to partner with other agents' LOAs, which means we literally cannot recruit you even if we tried.

Fill out the form below. 2 minutes. We review it, we hop on a call, we figure out which path fits. If it's a fit, we get to work. If it's not, we'll tell you. No obligation, either way.

Fill out the form. 2 minutes. We'll figure out which path fits and reach out within one business day. If it's not a fit, you'll hear that too. Either way, no obligation.

Google Ads vs. Facebook Ads for Annuity Lead Generation: Which One Works Better?

ACROPOLIS DIGITAL LLC | DECEMBER 2, 2024 | BY TREVOR BROWN

When it comes to generating leads for annuities, you might wonder whether Google Ads or Facebook Ads will deliver better results. Both platforms have their unique strengths and offer different approaches for reaching your ideal prospects. The key is understanding which platform works best for high-net-worth clients and high-intent leads—and how each can be leveraged to your advantage.

In this article, we’ll break down the pros and cons of Google Ads and Facebook Ads in the context of annuity marketing to help you make an informed decision.

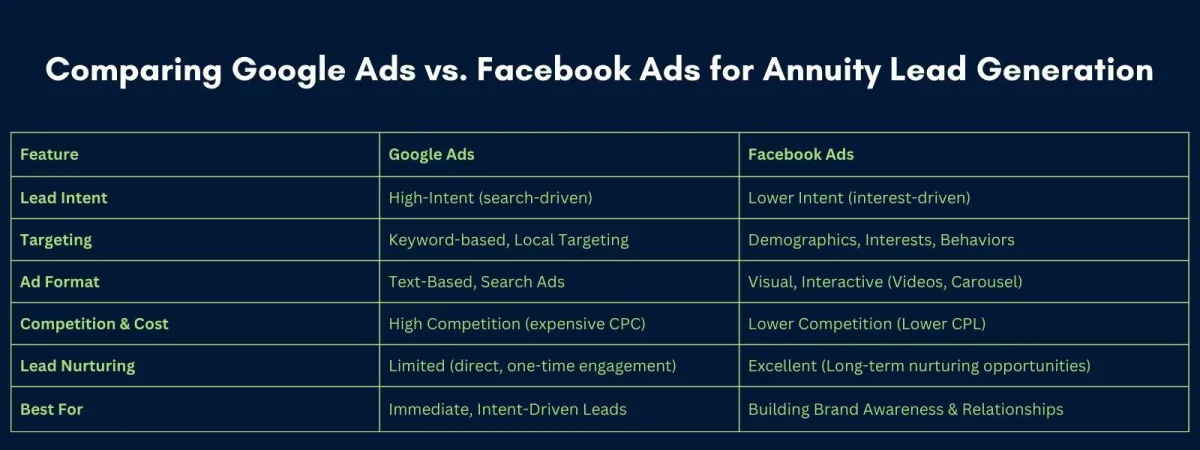

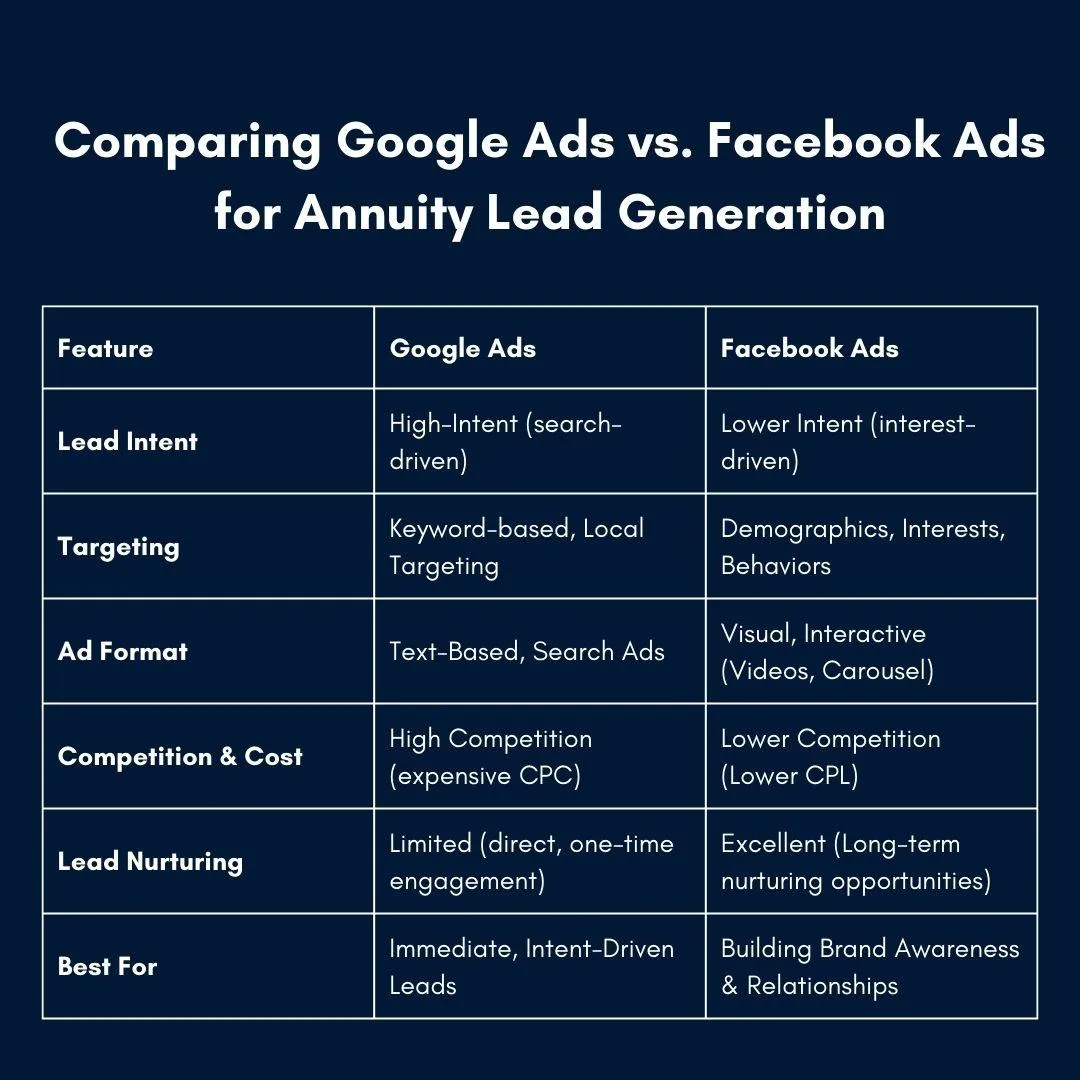

Google Ads for Annuity Lead Generation: Intent-Driven, Search-Based

How Google Ads Work

Google Ads are search-driven, meaning they show up when people actively search for something related to your product or service. With Google, people are typing in specific keywords like “best annuity rates” or “safe retirement options.” This shows that they already have a high intent to find solutions and make a decision.

Pros of Google Ads for Annuities

1. High-Intent Leads: Google Ads allows you to target people who are already searching for annuity-related products or retirement planning. These prospects are often further down the sales funnel and ready to engage.

2. Keyword Targeting: You can target highly specific keywords that focus on people actively seeking information about annuities, such as “fixed indexed annuities,” “best annuities for retirement,” or “guaranteed lifetime income.”

3. Local Targeting: If you're targeting a specific geographic region, Google Ads offers excellent local targeting options, allowing you to appear for searches like “annuity advisors in [your city]” for potential clients looking for a local expert.

4. Proven ROI: Google’s search ads generally have a strong track record of generating high-intent leads for industries like annuities, where prospects are actively researching options.

Cons of Google Ads for Annuities

1. High Competition and Cost: Annuity-related keywords are often highly competitive, especially when trying to rank for broader terms. Larger insurance carriers often dominate these searches, driving up costs per click (CPC).

2. Short-Term Focus: While Google Ads can drive immediate traffic, it doesn't necessarily build a long-term relationship with prospects. Once they click through, you have to quickly convert them into a lead or sale.

3. Complexity: Setting up and optimizing Google Ads campaigns requires a solid understanding of keyword research, ad copywriting, and budget management. Mistakes here can result in wasted ad spend.

Facebook Ads for Annuity Lead Generation: Visual and Behavioral Targeting

How Facebook Ads Work

Facebook Ads take a different approach by targeting people based on their interests, demographics, and behavioral data, rather than what they are actively searching for. On Facebook, you’re pushing ads to an audience that may not necessarily be searching for annuities but could benefit from learning about your products.

Pros of Facebook Ads for Annuities

1. Advanced Targeting: Facebook offers advanced targeting options where you can refine your audience based on their age, income, marital status, and interests (like retirement planning, investment, financial security, etc.). This makes it easier to target people likely to be interested in annuity products without relying on them actively searching for your services.

2. Custom Audiences: With Facebook, you can build custom audiences based on website visitors, email lists, or those who’ve interacted with your Facebook content. This helps you target people who are already familiar with your brand, increasing the chances of conversion.

3. Engaging Visuals: Facebook Ads are highly visual and can include videos, carousel ads, or single images to grab attention and explain complex annuity products in an easy-to-understand format. You can use these ads to build a connection with your audience, showcase success stories, and explain how annuities work in a way that resonates with them.

4. Lower Cost Per Lead (CPL): Compared to Google Ads, Facebook Ads can have a lower CPL, especially if you’re targeting niche groups or using Facebook’s Lead Generation Ads, which allow users to opt in directly within the app without leaving the platform.

5. Build Long-Term Relationships: Facebook Ads help you nurture potential clients over time. By running educational or informative ads, you can build trust and keep your brand top-of-mind as prospects begin their decision-making process.

Cons of Facebook Ads for Annuities

1. Lower Intent: Since Facebook Ads are shown to users based on interests and behaviors (not search intent), the audience may not be as actively engaged or ready to convert as those who use Google. This means you may need to work harder to nurture these leads into high-intent prospects.

2. Ad Fatigue: People on Facebook are constantly scrolling through their feeds. Your ads need to be creative and engaging to stand out. With time, ads can become stale, and it can be hard to maintain the same level of performance if the audience becomes disengaged.

3. Privacy Concerns: As social media platforms become more sensitive to privacy issues, targeting capabilities may become restricted in the future. This could affect your ability to reach high-net-worth individuals or narrow down your audience in specific ways.

Conclusion: Which Is Better for Annuities?

Both Google Ads and Facebook Ads have their strengths when it comes to generating leads for annuities. If you’re looking for high-intent, ready-to-purchase leads who are actively searching for annuity solutions, Google Ads may be the better choice. However, if you’re looking to target specific demographics, build brand awareness, and engage with a broader audience at a lower cost, Facebook Ads might be more effective.

In the end, the best approach is often a combination of both. You can use Google Ads to capture immediate intent and Facebook Ads to build a long-term relationship with potential clients. By leveraging the strengths of each platform, you can generate high-quality, exclusive, real-time leads for your annuity products.

Google Ads vs. Facebook Ads for Annuity Lead Generation: Which One Works Better?

ACROPOLIS DIGITAL LLC | NOVEMBER 22, 2024 | BY TREVOR BROWN

When it comes to generating leads for annuities, you might wonder whether Google Ads or Facebook Ads will deliver better results. Both platforms have their unique strengths and offer different approaches for reaching your ideal prospects. The key is understanding which platform works best for high-net-worth clients and high-intent leads—and how each can be leveraged to your advantage.

In this article, we’ll break down the pros and cons of Google Ads and Facebook Ads in the context of annuity marketing to help you make an informed decision.

Google Ads for Annuity Lead Generation: Intent-Driven, Search-Based

How Google Ads Work

Google Ads are search-driven, meaning they show up when people actively search for something related to your product or service. With Google, people are typing in specific keywords like “best annuity rates” or “safe retirement options.” This shows that they already have a high intent to find solutions and make a decision.

Pros of Google Ads for Annuities

1. High-Intent Leads: Google Ads allows you to target people who are already searching for annuity-related products or retirement planning. These prospects are often further down the sales funnel and ready to engage.

2. Keyword Targeting: You can target highly specific keywords that focus on people actively seeking information about annuities, such as “fixed indexed annuities,” “best annuities for retirement,” or “guaranteed lifetime income.”

3. Local Targeting: If you're targeting a specific geographic region, Google Ads offers excellent local targeting options, allowing you to appear for searches like “annuity advisors in [your city]” for potential clients looking for a local expert.

4. Proven ROI: Google’s search ads generally have a strong track record of generating high-intent leads for industries like annuities, where prospects are actively researching options.

Cons of Google Ads for Annuities

1. High Competition and Cost: Annuity-related keywords are often highly competitive, especially when trying to rank for broader terms. Larger insurance carriers often dominate these searches, driving up costs per click (CPC).

2. Short-Term Focus: While Google Ads can drive immediate traffic, it doesn't necessarily build a long-term relationship with prospects. Once they click through, you have to quickly convert them into a lead or sale.

3. Complexity: Setting up and optimizing Google Ads campaigns requires a solid understanding of keyword research, ad copywriting, and budget management. Mistakes here can result in wasted ad spend.

Facebook Ads for Annuity Lead Generation: Visual and Behavioral Targeting

How Facebook Ads Work

Facebook Ads take a different approach by targeting people based on their interests, demographics, and behavioral data, rather than what they are actively searching for. On Facebook, you’re pushing ads to an audience that may not necessarily be searching for annuities but could benefit from learning about your products.

Pros of Facebook Ads for Annuities

1. Advanced Targeting: Facebook offers advanced targeting options where you can refine your audience based on their age, income, marital status, and interests (like retirement planning, investment, financial security, etc.). This makes it easier to target people likely to be interested in annuity products without relying on them actively searching for your services.

2. Custom Audiences: With Facebook, you can build custom audiences based on website visitors, email lists, or those who’ve interacted with your Facebook content. This helps you target people who are already familiar with your brand, increasing the chances of conversion.

3. Engaging Visuals: Facebook Ads are highly visual and can include videos, carousel ads, or single images to grab attention and explain complex annuity products in an easy-to-understand format. You can use these ads to build a connection with your audience, showcase success stories, and explain how annuities work in a way that resonates with them.

4. Lower Cost Per Lead (CPL): Compared to Google Ads, Facebook Ads can have a lower CPL, especially if you’re targeting niche groups or using Facebook’s Lead Generation Ads, which allow users to opt in directly within the app without leaving the platform.

5. Build Long-Term Relationships: Facebook Ads help you nurture potential clients over time. By running educational or informative ads, you can build trust and keep your brand top-of-mind as prospects begin their decision-making process.

Cons of Facebook Ads for Annuities

1. Lower Intent: Since Facebook Ads are shown to users based on interests and behaviors (not search intent), the audience may not be as actively engaged or ready to convert as those who use Google. This means you may need to work harder to nurture these leads into high-intent prospects.

2. Ad Fatigue: People on Facebook are constantly scrolling through their feeds. Your ads need to be creative and engaging to stand out. With time, ads can become stale, and it can be hard to maintain the same level of performance if the audience becomes disengaged.

3. Privacy Concerns: As social media platforms become more sensitive to privacy issues, targeting capabilities may become restricted in the future. This could affect your ability to reach high-net-worth individuals or narrow down your audience in specific ways.

Conclusion: Which Is Better for Annuities?

Both Google Ads and Facebook Ads have their strengths when it comes to generating leads for annuities. If you’re looking for high-intent, ready-to-purchase leads who are actively searching for annuity solutions, Google Ads may be the better choice. However, if you’re looking to target specific demographics, build brand awareness, and engage with a broader audience at a lower cost, Facebook Ads might be more effective.

In the end, the best approach is often a combination of both. You can use Google Ads to capture immediate intent and Facebook Ads to build a long-term relationship with potential clients. By leveraging the strengths of each platform, you can generate high-quality, exclusive, real-time leads for your annuity products.

Featured

Marketing Maverick: Acropolis Digital’s...

Featured

The Acropolis Digital LLC Announces ...

Featured

Why Facebook, TikTok, and Instagram Lead Gen Is Better...

Featured

How Life Insurance Brokers Can Generate High-Quality Leads Using Video Ads...

Featured

Google Ads vs. Facebook Ads for Annuity Lead Generation: Which One Works Better?...

Featured

Facebook and Instagram vs. TikTok Ads for Life Insurance Brokers...

Featured

Turning Life and Annuity Clients into Referral Partners...

Featured

The Power of the Quiz Funnel for IUL and Annuity Lead Generation...

Featured

How to Generate Life Insurance Leads on TikTok...

Featured

Advanced EMA Marketing Strategies: How to Optimize & Scale...

Featured

Advanced SMS Marketing Strategies for Life Insurance & Annuity Sales...

Featured

Beginner-Friendly SMS Marketing Guide for Life Insurance & Annuity Sales...

Featured

Boost Your Life Insurance Sales...

Featured

How to Audit Your Own Tonality to 10X Your Life and Annuity Sales ...

Featured

How to get Free Life Insurance & Annuity Leads using Meetup & Alignable ...

Featured

How to Increase Your Life Insurance Commissions: Top 5 Strategies for Bigger Payouts...

Featured

How to Recruit Life Insurance Agents Using Meetup & Alignable (50+ Recruits Per Month)...

Featured

I Bought Jeremy Miner’s Course & Watched all 4,185 of His Reels – Here Are the Top 10 Lessons to Increase Your Life Insurance Sales...

Want to learn how?

Discover how the Acropolis Digital can help grow your annuity business.

Join Trevor for a quick, 30-minute video call to learn strategies that drive leads, streamline client acquisition, and boost your revenue.

Want to learn how?

Discover how the Acropolis Digital can help grow your annuity business.

Join Trevor for a quick, 30-minute video call to learn strategies that drive leads, streamline client acquisition, and boost your revenue.

Featured

Marketing Maverick: Acropolis Digital’s...

Featured

The Acropolis Digital LLC Announces ...

Featured

Why Facebook, TikTok, and Instagram Lead Gen Is Better...

Featured

How Life Insurance Brokers Can Generate High-Quality Leads Using Video Ads...

Featured

Google Ads vs. Facebook Ads for Annuity Lead Generation: Which One Works Better?...

Featured

Facebook and Instagram vs. TikTok Ads for Life Insurance Brokers...

Featured

Turning Life and Annuity Clients into Referral Partners...

Featured

The Power of the Quiz Funnel for IUL and Annuity Lead Generation...

Featured

How to Generate Life Insurance Leads on TikTok...

Featured

Advanced EMA Marketing Strategies: How to Optimize & Scale...

Featured

Advanced SMS Marketing Strategies for Life Insurance & Annuity Sales...

Featured

Beginner-Friendly SMS Marketing Guide for Life Insurance & Annuity Sales...

Featured

Boost Your Life Insurance Sales...

Featured

How to Audit Your Own Tonality to 10X Your Life and Annuity Sales ...

Featured

How to get Free Life Insurance & Annuity Leads using Meetup & Alignable ...

Featured

How to Increase Your Life Insurance Commissions: Top 5 Strategies for Bigger Payouts...

Featured

How to Recruit Life Insurance Agents Using Meetup & Alignable (50+ Recruits Per Month)...

Featured

I Bought Jeremy Miner’s Course & Watched all 4,185 of His Reels – Here Are the Top 10 Lessons to Increase Your Life Insurance Sales...

©2024 & Beyond theacropolisdigital.com

Copyright Acropolis Digital LLC, all Rights Reserved.

©2024 & Beyond theacropolisdigital.com

Copyright Acropolis Digital LLC, all Rights Reserved.